A credit evaluation agent reads, cross-checks and flags loan documents — a human still makes the lending decision.

A credit evaluation agent is an AI system that reads a loan applicant's documents, cross-checks them against each other, and flags the discrepancies — so a human credit officer spends their time deciding, not matching. Here is how it works, where the human stays in control, and how a Malaysian lender deploys one compliantly.

A credit team at a Klang Valley motorcycle financier — we'll call them MotoKredit (name changed) — described their bottleneck to us in one sentence: "Most of our reviewers' day is spent checking that documents agree with each other, not deciding whether to lend."

Every hire-purchase application lands as a bundle — an IC, three months of payslips, six months of bank statements, the dealer's quotation, and a signed financing form. A reviewer opens each one, reads it, and cross-checks it against the rest by eye. Does the name on the payslip match the IC and the application? Does the declared income actually show up as salary credits in the bank statement? Is the account on the statement the same one on the form? Are all six months present, or is one missing? Only after all that mechanical matching is done does the real judgement — should we approve this? — begin.

That first, mechanical layer is exactly what a credit evaluation agent takes over. This article is the detailed version of what we proposed to MotoKredit, written so you can judge whether it fits your own lending operation — whether you run hire-purchase, personal financing, a co-operative, a licensed moneylender, or a BNPL book.

What a credit evaluation agent actually does

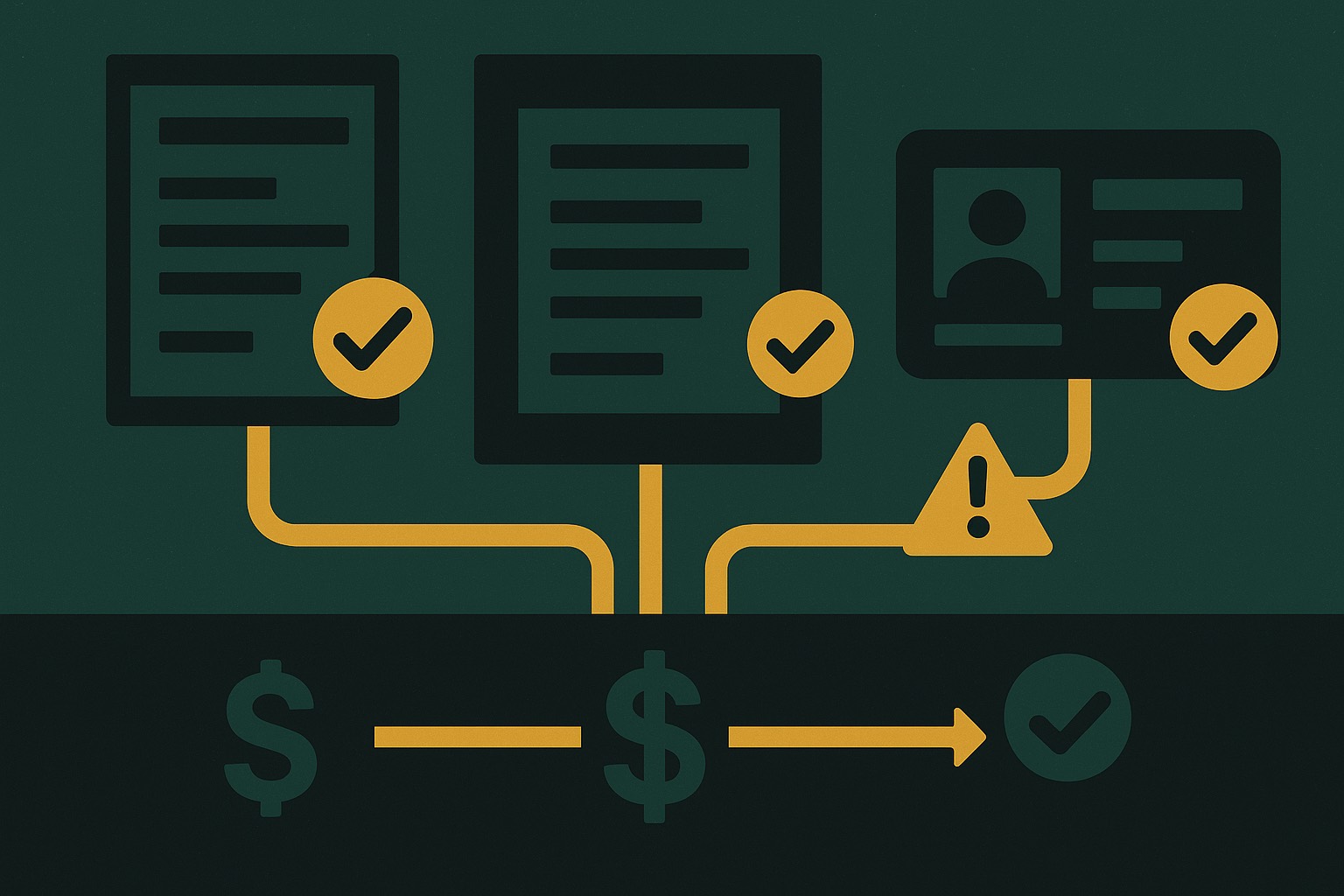

It helps to be precise, because "AI credit scoring" and "credit evaluation agent" are not the same thing. A credit score model outputs a number. An agent does work: it reads unstructured documents, reconciles them, and produces a reviewable summary. Concretely, for each application it:

- Reads every document — including scans and phone photos — and extracts the fields that matter: name, IC number, employer, declared income, bank account, monthly commitments.

- Cross-checks and matches those fields across the bundle: name on IC vs payslip vs application; declared income vs the actual pattern of salary credits; the statement's account vs the form's; whether the required months of statements are all present.

- Flags discrepancies with the specific figures and the document they came from — a name mismatch, an income gap, a missing statement month, an account that appears nowhere else, signs of a doctored document.

- Hands the officer a one-page summary — the applicant, the checks that passed, and the two or three things worth a closer look, each with its evidence.

What lands on the credit officer's desk is no longer a stack of raw PDFs. It's a structured file with the mechanical work already done and the exceptions surfaced. This is the same document comparison and matching pattern behind custom AI agent development — pointed squarely at credit.

Where the human stays in control (this part is not optional)

A credit evaluation agent does not approve or decline anyone. It does the reading, matching and flagging; the lending decision stays with a person. For any regulated lending activity in Malaysia, that human-in-the-loop design isn't a nicety — it's how you stay accountable and auditable. Bank Negara Malaysia's responsible financing expectations assume a lender can explain and stand behind each decision; an agent that quietly auto-approved applications would undermine exactly that. (This is general information, not compliance advice — confirm your obligations with your own counsel and, where relevant, BNM guidance.)

Two design choices make this real:

- Evidence, not verdicts. Every flag points to the document and the figure behind it, so the officer verifies rather than trusts a black box.

- A full audit trail. What the agent read, extracted and flagged is logged, so a decision can be reconstructed months later for an internal review or a regulator.

Handling sensitive data properly

Credit files are about as sensitive as data gets — IC numbers, payslips, bank statements. Any credit evaluation agent has to be built around Malaysia's personal data protection rules (PDPA): clear answers on where data is processed and stored, retention limits, and access controls. This is a large part of why lenders build a custom agent with a partner rather than piping applicant documents through a generic public tool — you need to know exactly where the data goes.

The build, in plain terms

Under the hood this leans on three capabilities, none of which you need to write yourself:

- Document understanding — modern Anthropic models read text, tables and scanned images and extract meaning, not just characters (Anthropic Claude).

- Agent orchestration — the Claude Agent SDK runs the loop: read, cross-check, decide what to verify next, and stop when a human is needed.

- System connections — the Model Context Protocol (MCP) connects the agent to your loan origination system and document store safely and reversibly.

The work is in designing the checks around your products, your documents and your risk policy, then testing against real historical files — including the messy and the fraudulent — until it's reliable. For a single, focused product line, that's a project measured in weeks, not months.

What changes when it works

We're deliberately not quoting a headline percentage — the honest measure depends on your volume and current process. But the pattern from the review is consistent:

- Reviewers spend their time on judgement, not matching. The mechanical cross-checking that ate the morning is done before the file reaches them.

- Consistency improves. The hundredth check of the afternoon is as thorough as the first, and two officers see the same flags rather than applying slightly different diligence.

- Throughput rises without adding headcount — the same team clears more files, because the slow part is automated.

- Fewer things slip through — a missing statement month or a mismatched account is caught every time, not just when someone's paying close attention.

None of that replaces the credit officer. It removes the tedious layer beneath them.

Is this only for motor financing?

No — MotoKredit's problem isn't really about motorcycles. Strip out the product and it's: read a set of related financial documents, reconcile them, flag what doesn't add up, escalate to a human. That shape recurs across lending and beyond — personal financing and co-operatives, BNPL underwriting, SME trade finance, and, with different documents, insurance claims and KYC onboarding. Build the credit evaluation agent once, and you have a template for the next document-heavy review. It's one application of the broader agentic workflow automation shift, delivered as a custom AI agent.

Frequently asked questions

What is a credit evaluation agent? An AI agent that reads a loan applicant's documents, cross-checks them against each other, and flags discrepancies for a human credit officer. It automates the document-matching layer of credit review — not the lending decision itself.

Does a credit evaluation agent approve or reject loans? No. It reads, matches and flags; a human makes the approve/decline decision. For regulated lending in Malaysia, keeping a person accountable for each decision (human-in-the-loop) is essential.

Is it compliant with BNM and PDPA? It's designed to be — with a full audit trail so decisions can be reconstructed, and built around PDPA requirements for where credit data is processed, stored and accessed. Treat this as a starting point for your compliance team, not legal advice.

What documents can it read? Typically ICs, payslips, bank statements, financing forms and dealer quotations — including scans and phone photos — extracting and cross-matching the fields that matter.

How long does it take to deploy? For a single, focused product line, a proof-of-concept is usually a matter of weeks; a full rollout takes longer, mostly because of integration and getting reviewers comfortable, not the AI.

Sources

- Claude Agent SDK — overview, Anthropic

- Model Context Protocol, the open standard for connecting agents to systems

- Claude, Anthropic (document understanding)

- Protection of Personal Data (PDPA), MyGovernment portal

- Bank Negara Malaysia responsible financing expectations (general reference — confirm current guidance with BNM and your compliance counsel)

Free consultation

Is your credit team spending its day matching documents?

If reviewers spend more time checking that payslips, statements and ICs agree than actually deciding, that's exactly what a credit evaluation agent takes over — with your officers keeping the decision. Tell us your product line and volumes, and we'll tell you honestly whether it's worth building.

The MotoKredit example is based on a real proof-of-concept engagement; the company name has been changed and details generalised at the client's request. Anchor Sprint is a member of the Anthropic Claude Partner Network — a deployment and rollout partner, not a reseller — and is not affiliated with, authorized by, or endorsed by Anthropic; Claude and Anthropic are trademarks of Anthropic, PBC. This article is general information, not legal, compliance or lending advice; confirm your PDPA and Bank Negara Malaysia obligations with your own counsel.